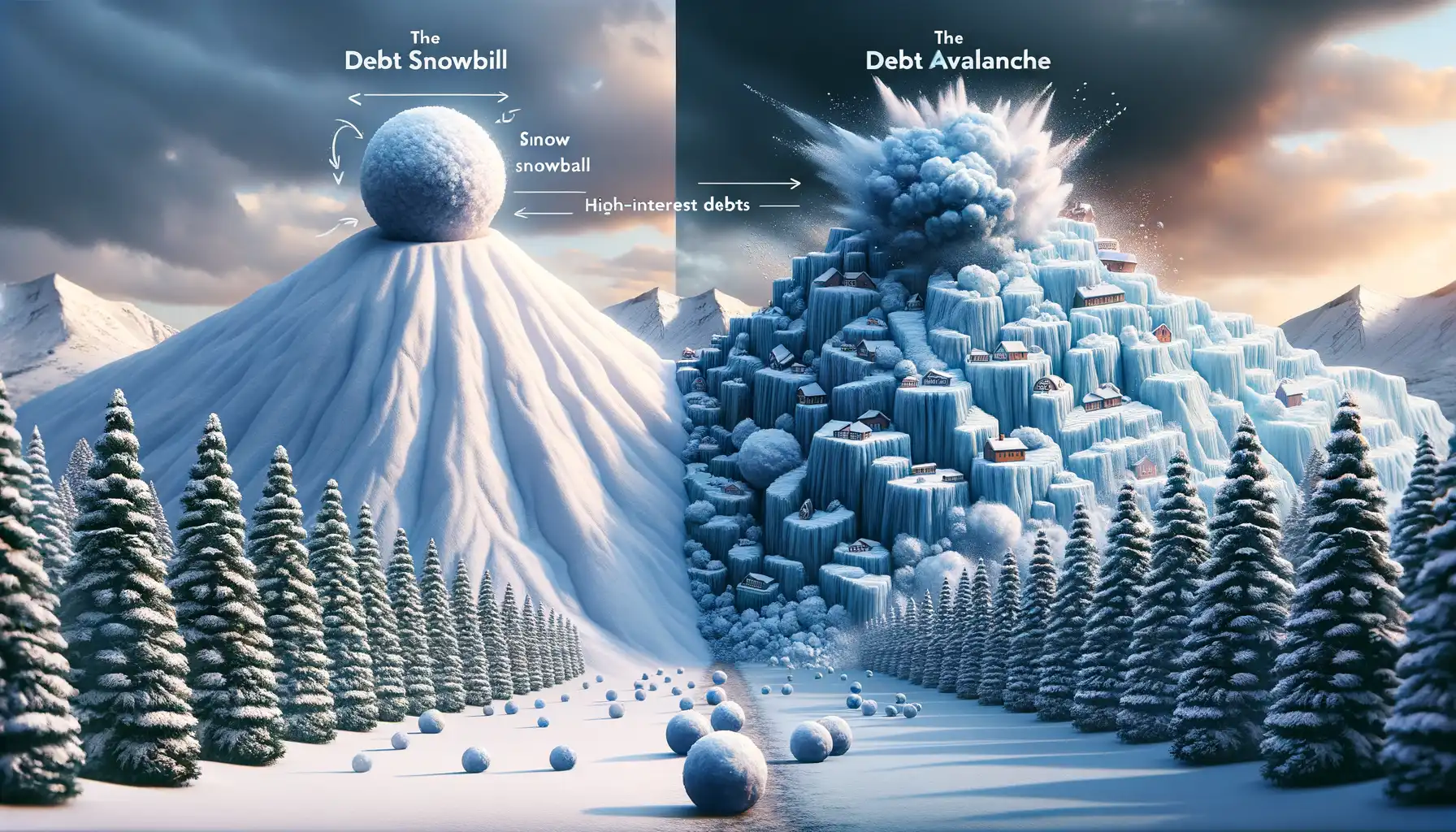

Understanding the Debt Snowball Method

Feeling overwhelmed by debt? Let’s talk about the Debt Snowball Method, a strategy that’s less about math and more about psychology—breaking down the big, scary mountain of debt into manageable snowballs. Picture this: instead of staring at all your debts and feeling stuck, you start with the smallest one and go from there. Success builds momentum, just like when you finally say “yes” to hitting the gym—or eating that first bite of cake. (Hey, we’re all human.)

Why Starting Small Can Lead to Big Wins

This method focuses on getting those small victories under your belt first. Let’s break it down:

- List all your debts from smallest to largest, ignoring interest rates for now.

- Pay off the minimum balance on everything except the smallest debt—this one gets your full attention.

- Once that first debt is crushed, roll whatever payment you were making into the next smallest debt. Rinse and repeat.

It’s like knocking over dominoes. One falls, then another, and soon, the whole row collapses. And with each win, you feel stronger, more in control, and ready to tackle even bigger financial challenges.

The Real Power of Momentum

The genius of the Debt Snowball Method is how it reshapes your mindset. Imagine crossing off a debt like crossing a finish line—it’s electrifying. Sure, it might not be the most “mathematically perfect” method (more on that in our avalanche discussion), but for many, it’s the spark they need to stay motivated. Each zero balance feels like a tiny revolution against the bills that once ruled your life. And trust us—those victories add up fast.

Exploring the Debt Avalanche Method

How the Debt Avalanche Method Works

Picture this: you’re standing at the base of a massive mountain of debt. It’s intimidating. But what if you had a strategy that struck the heart of those high-interest rates first, melting away your financial stress? That’s exactly what the Debt Avalanche Method promises.

With this approach, you focus on paying off debts with the highest interest rate first, regardless of their balance size. Why? Because high-interest debt devours your money like an insatiable beast. Credit cards at 22% APR? Those are the villains you’ll tackle head-on before worrying about smaller, lower-interest loans.

- Step 1: Organize debts from highest to lowest interest rate.

- Step 2: Pay the minimum on all debts except the one with the highest rate.

- Step 3: Funnel every spare penny toward that costly debt until it’s obliterated.

Why It’s a Game-Changer

The beauty of the Avalanche is its efficiency. While it might not give you the instant gratification of quick victories (hello, Debt Snowball), it slashes the total interest paid over time. Imagine saving hundreds—or even thousands—of dollars simply by tackling debts smarter, not harder.

Picture this: instead of chipping away at chucklesome $200 debts, you’re defeating the real villains—a $10,000 credit card debt at 25%. Once that giant is slain, the relief feels monumental. The view from the top of this mountain? Financial freedom. And it’s breathtaking.

Key Differences Between Debt Snowball and Debt Avalanche

How Each Method Tackles Debt Differently

When it comes to paying off debt, a one-size-fits-all approach doesn’t exist. Both the Debt Snowball and the Debt Avalanche are powerful strategies, but their paths couldn’t be more different—it’s like choosing between hiking a scenic trail or racing down a steep hill.

The Debt Snowball focuses on psychology. It pumps you full of motivation by prioritizing your smallest balances first. You pay minimums on all debts except the tiniest one, which you attack with every spare dollar. Why? Because knocking out a small balance feels incredible. That “paid in full” moment is like an espresso shot for your confidence!

Debt Avalanche, on the other hand, is all about mathematics. It zooms in on debts with the highest interest rates, tackling those first to save money long-term. While it’s less emotionally charged, this approach chips away at the financial drain of compounding interest—your biggest enemy.

- Snowball = Quick wins, keeps you fired up.

- Avalanche = Strategic and interest-saving.

Both have their charm, so the real question is: Do you need quick emotional wins or are you laser-focused on minimizing dollars spent?

Factors to Consider When Choosing Your Debt Payoff Strategy

What Drives You? Emotions vs. Logic

When it comes to paying off debt, your personality and mindset play a HUGE role. No two people approach this journey the same way, and that’s a good thing. Ask yourself: Are you someone who thrives on small victories to keep the momentum alive? If so, the Debt Snowball method might feel like a confidence-boosting celebration every time you knock out a bill. On the other hand, if you’re laser-focused on numbers and want the biggest bang for your buck, the Debt Avalanche might be your ideal match—it’s all about saving money on interest in the long run.

Your Financial Reality Check

Facing your finances head-on is the hard part, but it’s also where clarity comes in. Here are a few practical considerations to help steer your decision:

- Interest Rates: Carrying high-interest debts? The Avalanche can crush those costs faster.

- Debt Sizes: Tackling tiny balances first with the Snowball can give you instant wins (like a shot of espresso for your determination!).

- Budget Flexibility: Can you handle fluctuating payments as you prioritize higher-interest debts?

- Emotional Resilience: Do you need motivation boosters or prefer the logical path?

No strategy is one-size-fits-all. The magic happens when you align your plan with what truly speaks to you—whether that’s emotional rewards, financial logic, or maybe even a blend of both!

Tips for Staying Motivated and Achieving Financial Freedom

Breathe Life Into Your Financial Goals

Breaking free from debt can sometimes feel like climbing a steep mountain, but remember—you’re not alone on this journey. Staying motivated is like keeping a fire lit; it needs kindling and care. One powerful way to stay focused is to remind yourself of *why* you’re doing this. Is it to give your family a more secure home? To travel the world? Picture that—vividly. Put it where you can see it daily: a vision board, a sticky note on your mirror, or even the lock screen on your phone.

And don’t forget to celebrate small wins along the way! When you pay off that first credit card or knock out a chunk of your student loans, treat yourself (within reason). Buy your favorite coffee or enjoy a night in with a movie you love.

- Create milestones instead of focusing solely on the finish line.

- Reward progress—because every step forward is worth celebrating.

- Track your victories visually, like coloring in a chart as you pay down balances.

The Power of Connection

Debt can be lonely, but it doesn’t have to be. Share your goals with someone who gets it—a partner, friend, or even an online community. Lean on them when doubt sneaks in. Ever heard the saying, “Iron sharpens iron”? Surrounding yourself with people on similar financial journeys can work wonders for your morale.

Lastly, never underestimate the power of self-compassion. Paying off debt is tough. There will be off days, unexpected expenses, and moments when motivation wavers. That’s normal. Dust yourself off, forgive slip-ups, and refocus on that brighter, debt-free future. You’ve got what it takes—step by step, dollar by dollar.